I think this case decision should be studied. While it is easy to be dismissive of emotional distress damages, this case clearly enunciates the basis for it. I think we tend to demote the claim because of the underlying bias that the borrower has been getting a “free ride.” This case states quite clearly that the ride was neither wanted nor free.Perhaps just as importantly, the Court finds that punitive damages are appropriate in order to get the attention of Bank of America — such that it will stop it’s malevolent behavior. It sets the bar at deterring the bank from this behavior and not just a “cost of doing business.”

For those who don’t think we have turned the corner, this case shows clearly that judges are not allowing themselves to be spoon-fed the diet of illusion, smoke and mirrors that has prevailed so long in the American court system. If these decisions were made 10 years ago we would not have had a foreclosure crisis.

==================================

KM Writes:

This is an interesting new FDCPA decision. The judge found that BANA violated the FDCPA and awarded 50k/each to husband and wife for compensatory damages, based mainly on emotional distress as proved by the consumers’ testimony of anxiety, frustration, and sleeplessness. Also, he awarded $100,000 in punitives under the FDCPA, even given a very stringent Florida statute, because BANA’s negligence was gross, by a clear and convincing standard, primarily because the debtors tried to fix the discrepancy numerous times, but the bank did not fix it, and initiated foreclosure. The “Bank employees were inattentive, unconcerned and haphazard,” but more importantly, in taking no action to prevent errors from continuing, despite repeated notice, “the Bank employees’ conduct was so wanting in care that it constituted a conscious disregard and indifference to the Goodins’ rights. It was as if the Goodins did not exist.” And it was “only stopped by the filing of this federal lawsuit.” Moreover, in creating a system where one Bank department did not communicate with another, where there were inadequate internal controls to ensure statements provided correct information, and where there was no way for Bank customers to get the attention of the Bank to correct the Bank’s errors, the Bank engaged in grossly negligent conduct. As such, it should be held liable for punitive damages for its employees’ gross negligence.”

Other interesting snippets:

As we know, BANA is a debt collector if “acquired the loan at issue while the loan was in default.”

Bank of America contends, however, that it is not a debt collector. A mortgage servicing company is a debt collector under the FDCPA if it acquired the loan at issue while the loan was in default. Williams v. Edelman, 408 F.Supp.2d 1261, 1266 (S.D.Fla.2005). Under the terms of their note, the Goodins were in default if they missed two or more consecutive payments. (Doc. 75 at 15). When Bank of America took over their loan, the Goodins had previously missed two or more consecutive payments and remained behind by more than two payments. (Trial Tr. vol. I at 30). Nevertheless, Bank of America argues that the Goodins were not in default because their bankruptcy plan cured any pre-existing default and the Goodins never defaulted on any payment due under the bankruptcy plan.7 (Doc. 101 at 6).

*5 While a bankruptcy plan may “provide for the curing or waiving of any default,” this does not mean, as Bank of America argues, that the entry of a bankruptcy plan itself cures a default. See11 U.S.C. § 1322(b)(3) (2014). Indeed, the bankruptcy statute also provides that the plan may “provide for the curing of any default within a reasonable time and maintenance of payments while the case is pending on any unsecured claim or secured claim on which the last payment is due after the date on which the final payment under the plan is due ….“ § 1322(b)(5). This provision suggests what is common sense: that the curing of the default occurs upon the repayment of the back payments owed, not upon the mere institution of the bankruptcy plan. See In re Agustin, 451 B.R. 617, 619 (Bankr.S.D.Fla.2011) (“Using [§ ] 1322(b)(5), the Debtors are able to cure arrearages over a time period exceeding the life of the Chapter 13 Plan.”); see also In re Alexander, 06–30497–LMK, 2007 WL 2296741 (Bankr.N.D.Fla. Apr.25, 2007) (finding it reasonable to cure a default over the five-year life of the bankruptcy plan). Bank of America is a debt collector.

Goodin v. Bank of Am., N.A., No. 3:13-CV-102-J-32JRK, 2015 WL 3866872, at *4-5 (M.D. Fla. June 23, 2015)

Act “in connection with the collection of a debt” only must have “animating purpose” to induce payment:

To be “in connection with the collection of a debt,” a communication need not make an explicit demand for payment. Grden v. Leikin Ingber & Winters PC, 643 F.3d 169, 173 (6th Cir.2011). However, “an animating purpose of the communication must be to induce payment by the debtor.”Id.; see also McIvor v. Credit Control Servs., Inc., 773 F.3d 909, 914 (8th Cir.2014); cf. Caceres v. McCalla Raymer, LLC, 755 F.3d 1299, 1303 n. 2 (11th Cir.2014) (noting that an implicit demand for payment constituted an initial communication in connection with a debt). Where a communication is clearly informational and does not demand payment or discuss the specifics of an underlying debt, it does not violate the FDCPA. Parker v. Midland Credit Mgmt., Inc., 874 F.Supp.2d 1353, 1358 (M.D.Fla.2012).

*6 Some of the communications alleged to be FDCPA violations did not have the animating purpose of inducing the Goodins to pay a debt. Specifically, Bank of America’s October 8, 2010 notice that the Goodins may be charged fees while their loan is in default status (Pl.’s Ex. 5), the December 3, 2010 letter alerting the Goodins to the existence of a program to avoid foreclosure despite their “past due” home loan payment (Pl.’s Ex. 6),9 the refusal to accept an alleged partial payment (Pl.’s Ex. 17), and the notice that the Goodins’ loan had been referred to foreclosure (Pl.’s Ex. 27), did not ask for or encourage payment and were not intended to induce payment. Likewise, the Bank of America branch employee’s refusal to accept Mr. Goodin’s payment was not an act in connection with the collection of a debt.

A regular bank statement sent only for informational purposes is also not an action in connection with the collection of a debt. See Helman v. Udren Law Offices, P.C., No. 0:14–CV–60808, 2014 WL 7781199, at *6 (S.D.Fla. Dec.18, 2014). As such, the Goodins’ November 10, 2009 account statement, which did not have the purpose of inducing payment from the Goodins, was not an FDCPA violation. (See Pl.’s Ex. 4 at 5).

The letter Bank of America’s counsel sent to the Goodins on October 25, 2013 (Joint Ex. 11) was likewise not an FDCPA violation because it did not falsely represent the amount or status of the Goodins’ debt, did not threaten an action Bank of America could not or did not intend to take, and did not constitute the use of a false representation or deceptive means in an attempt to collect a debt.

Goodin v. Bank of Am., N.A., No. 3:13-CV-102-J-32JRK, 2015 WL 3866872, at *5-6 (M.D. Fla. June 23, 2015)

Foreclosure as debt collection activity, only if seeks deficiency judgment

The lone remaining alleged violation is Bank of America’s filing of a foreclosure complaint against the Goodins. (Pl.’s Ex. 28). Foreclosing on a home is the enforcement of a security interest, not debt collection. Warren v. Countrywide Home Loans, Inc., 342 F. App’x 458, 461 (11th Cir.2009). However, a deficiency action does constitute debt collection activity.Baggett v. Law Offices of Daniel C. Consuegra, P.L., No. 3:14–CV–1014–J–32PDB, 2015 WL 1707479, at *5 (M.D.Fla. Apr.15, 2015). Communication that attempts to enforce a security interest may also be an attempt to collect the underlying debt. Reese v. Ellis, Painter, Ratterree & Adams, LLP, 678 F.3d 1211, 1217–18 (11th Cir.2012).

When a foreclosure complaint seeks a deficiency judgment if applicable, it attempts to collect on the security interest and the note. Roban v. Marinosci Law Grp., No. 14–60296–CIV, 2014 WL 3738628 (S.D.Fla. July 29, 2014). As such, two cases have found that foreclosure complaints that ask for a deficiency judgment “if applicable” constitute debt collection activity under the FDCPA. See id.; Rotenberg v. MLG, P.A., No. 13–CV–22624–UU, 2013 WL 5664886, at *2 (S.D.Fla. Oct.17, 2013). Similarly, a foreclosure complaint constitutes debt collection activity where it requests “that the court retain jurisdiction to enter a deficiency decree, if necessary.”Freire v. Aldridge Connors, LLP, 994 F.Supp.2d 1284, 1288 (S.D.Fla.2014).

Goodin v. Bank of Am., N.A., No. 3:13-CV-102-J-32JRK, 2015 WL 3866872, at *7 (M.D. Fla. June 23, 2015)

What they knew and when they knew it

At least two people in the Bank, Duane Dumler and Leslie Hodkinson, knew long before Mr. Juarez’s error that the Bank needed to file a transfer of claim to obtain the missing funds. Either because of the Bank’s size, because its departments were compartmentalized and did not properly communicate with each other, or some other reason, this knowledge did not make its way to the foreclosure department or to the part of the Bank responsible for sending out the communications that violated the FDCPA. Then, after Mr. Juarez’s negligent audit, the Goodins’ attorney contacted Bank of America to fix the problem, but the Bank still proceeded to misrepresent the amount the Goodins owed and ultimately filed a foreclosure complaint, only dismissing the foreclosure action after the Goodins literally had to make a federal case out of it.

Goodin v. Bank of Am., N.A., No. 3:13-CV-102-J-32JRK, 2015 WL 3866872, at *9 (M.D. Fla. June 23, 2015)

Factual Evidence of Emotional Damages; No Doctor Testimony Necessary

Since Bank of America began servicing the Goodins’ loan, Mrs. Goodin has felt anxious every day, worrying about the status of her loan. (Id. at 239–40). At times, she has lost sleep because of her concern about the loan. (Id. at 240). However, she never went to a doctor for treatment, in part because she did not have insurance to do so and in part because she did not believe a doctor would make a difference. (Id. at 241).

Mr. Goodin likewise suffered anxiety and sleeplessness as a result of Bank of America’s improper servicing. (Trial Tr. vol. II at 105). Mr. Goodin was immensely frustrated by Bank of America’s lack of responsiveness to his attempts to fix the problems with his loan. (Id. at 74). He sent letters, talked to a Bank of America employee face-to-face, and tried everything that he could think of, but could not find a way to get Bank of America to file the transfer of claim or correct its servicing of the Goodins’ loan. (Id. at 74). While Mr. Goodin’s description of his life as “a pure living hell” is perhaps hyperbolic, it is clear that Bank of America’s letters and Mr. Goodin’s inability to correct the problem made him feel powerless and caused him considerable anger and distress. (See id. at 74, 86).

Most of the Goodins’ testimony dealt generally with emotional distress they suffered throughout the Bank’s servicing of their loan. However, Mrs. Goodin was especially concerned when the Goodins’ bankruptcy was discharged because Bank of America was not getting their payments and she knew that, absent payment, Bank of America would take legal action against them. (Id. at 18). The Goodins noted that they also suffered particular stress upon being served with the foreclosure complaint. (Id. at 79). The possibility of losing their home to foreclosure upset Mr. Goodin and left Mrs. Goodin worried and scared. (Id. at 79).

Bank of America was not the only cause of stress in the Goodins’ lives. Mrs. Goodin was under stress before they filed for bankruptcy because the Goodins were having trouble paying their bills. (Id. at 13). She also suffered the loss of her mother around 2011. (Id. at 69). In June 2013, the Goodins sued TRS Recovery Services, Bennett Law, PLLC, and Wal–Mart (Id. at 22), alleging that they were the victims of check fraud in September 2011 (Id. at 24). Because of the wrongful debt incurred by the fraud, TRS sent the Goodins collection letters from October 2011 through November 2012 and called frequently from October 2011 until July 2012. (Id. at 24–25). As a result, the Goodins lost sleep, felt anxious, and suffered other symptoms of emotional distress. (Id. at 26). However, the Goodins testified credibly that the stress, anxiety, and sleeplessness caused by the events underlying the TRS lawsuit pale in comparison to the emotional distress the Goodins suffered as a result of Bank of America’s actions. (Id. at 64, 106).

*11 While not accepting every aspect of their testimony, overall, the Court found the Goodins’ testimony regarding the emotional distress caused by the Bank’s FDCPA and FCCPA violations to be believable. The tumult of receiving repeated erroneous communications from the Bank, their inability to get anybody at the Bank to listen to them, their feelings of loss of control and the very real fear of losing their home combined to create a very stressful situation.

Goodin v. Bank of Am., N.A., No. 3:13-CV-102-J-32JRK, 2015 WL 3866872, at *10-11 (M.D. Fla. June 23, 2015)

- THE COURT’S DECISION ON DAMAGES

- Statutory Damages

Under both the FDCPA and FCCPA, prevailing plaintiffs are entitled to statutory damages of up to $1,000. 15 U.S.C. § 1692k; Fla. Stat. § 559.77. In determining the appropriate amount, the Court must consider “the frequency and persistence of noncompliance by the debt collector, the nature of such noncompliance, and the extent to which such noncompliance was intentional ….“ 15 U.S .C. § 1692k; see alsoFla. Stat. § 559.77(2). Upon consideration of the Bank’s repeated statutory violations and inability to correct the problems with the Goodins’ loans despite a plethora of chances to do so, the Court finds Mr. and Mrs. Goodin are each entitled to $1,000 under the FDCPA and $1,000 under the FCCPA.

- Actual Damages

The Goodins also each seek $500,000 in actual damages to compensate for their emotional distress. (Doc. 100–1 at 17). A plaintiff may recover actual damages for emotional distress under the FDCPA and FCCPA. Minnifield v. Johnson & Freedman, LLC, 448 F. App’x 914, 916 (11th Cir.2011) (finding that a plaintiff can recover for emotional distress under the FDCPA); Fini v. Dish Network L.L.C., 955 F.Supp.2d 1288, 1299 (M.D.Fla.2013) (finding the same under the FCCPA).

In determining what actual damages are appropriate in this case, the Court has only considered those damages caused by the Bank’s FDCPA and FCCPA violations, and not any distress caused by other aspects of the Bank’s improper servicing of the Goodins’ account. To recap, Bank of America violated the FDCPA when it (1) mailed ten statements from April 25, 2011 to March 29, 2012, indicating, amongst other misstatements, an overstated balance on the loan; (2) mailed statements in March and August 2011 misstating that the Goodins owed foreclosure fees; (3) sent the Goodins six letters between December 27, 2011 and March 16, 2012 requesting over $15,000 in payments and threatening to accelerate the debt or foreclose in the absence of payment; and (4) filed a foreclosure complaint on September 17, 2012. Any emotional distress the Goodins suffered as a result of the Bank’s violations therefore occurred between March 2011, the date of the first violation, and October 2013, when the Bank finally corrected its servicing errors.

“Emotional distress must have a severe impact on the sufferer to justify an award of actual damages.”Alecca v. AMG Managing Partners, LLC, No. 3:13–CV–163–J–39PDB, 2014 WL 2987702, at *2 (M.D.Fla. July 2, 2014). As such, a number of courts have declined to award damages for emotional distress where the plaintiff’s testimony was not supported by medical bills. See, e.g., Lane v. Accredited Collection Agency Inc., No. 6:13–CV–530–ORL–18, 2014 WL 1685677, at *8 (M.D.Fla. Apr.28, 2014) (adopting a report and recommendation recommending no actual damages despite testimony that the plaintiff suffered nervousness, anxiety, and sleeplessness); compare Marchman v. Credit Solutions Corp., No. 6:010–CV–226–ORL–31, 2011 WL 1560647, at *10 (M.D.Fla. Apr.5, 2011)report and recommendation adopted,No. 6:10–CV–226–ORL–31, 2011 WL 1557853 (M.D.Fla. Apr.25, 2011) (awarding no actual damages where the plaintiff testified that she spent nights awake with worry and was withdrawn and depressed but did not provide evidence she required medical or professional services) with Latimore v. Gateway Retrieval, LLC, No. 1:12–CV–00286–TWT, 2013 WL 791258, at *10–11 (N.D.Ga. Feb.1, 2013)report and recommendation adopted,No. 1:12–CV–286–TWT, 2013 WL 791308 (N.D.Ga. Mar.4, 2013) (awarding $10,000 in emotional distress damages where the plaintiff submitted medical bills to support her testimony). Indeed, both courts and juries have rejected claims for emotional distress in cases involving serious FDCPA violations. See Montgomery v. Florida First Fin. Grp., Inc., No. 6:06–CV–1639ORL31KR, 2008 WL 3540374, at *9 (M.D.Fla. Aug.12, 2008) (adopting a Report and Recommendation recommending no actual damages despite the defendant threatening six times, to plaintiff, plaintiff’s daughter, and plaintiff’s mother, that it would have plaintiff arrested, and despite plaintiff’s testimony she was scared and struggled to sleep for fear that she would be arrested); Jordan v. Collection Services, Inc., Case No. 97–600–CA–01, 2001 WL 959031 (Fla. 1st Cir. Ct. April 5, 2001) (jury awarded no damages despite defendant’s debt collection calls that threatened, amongst other consequences, that a hospital would refuse to admit plaintiffs’ ill child if they did not pay their debt).

*12 Still, other courts have awarded actual damages for emotional distress for FDCPA and FCCPA violations, albeit usually in relatively small amounts. For example, in Barker v. Tomlinson, No. 8:05–CV–1390–T–27EAJ, 2006 WL 1679645 (M.D.Fla. June 7, 2006), the plaintiff received $10,000 in actual damages where the defendant called her at work to demand payment for an illegitimate debt, threatened her with arrest if she did not pay, and faxed a request for an arrest warrant to her workplace. Barker, at *3. Similarly, where the plaintiff suffered three panic attacks after the defendant threatened that she could go to jail, threatened to send a deputy to her house, and told her daughter that her mom would be arrested, the court awarded $1,000 in actual damages.Rodriguez v. Florida First Fin. Grp., Inc., No. 606CV–1678–ORL–28DAB, 2009 WL 535980, at *6 (M.D.Fla. Mar.3, 2009).

There are two notable exceptions to the small damages awards usually given in FDCPA cases. In Mesa v. Insta–Service Air Conditioning Corp., Case No. 03–20421 CA 11, 2011 WL 5395524 (Fla. 11th Cir.Ct. Aug. 2, 2011), a jury awarded $150,000 in compensatory damages where an air conditioning company defrauded the plaintiff into buying a defective air conditioner and, unbeknownst to the plaintiff, took out a line of credit in his name. However, it is unclear what amount of those compensatory damages were based on emotional distress and what amount were economic damages. In Beasley v. Anderson, Randolf, Price LLC, Case No. 16–2007–CA–005308, 2010 WL 6708036 (Fla. 4th Cir. Ct. April 19, 2010), a jury awarded $75,000 for mental anguish, inconvenience, or loss of capacity for the enjoyment of life after the defendant repeatedly called the plaintiff’s cell phone to collect a debt, even after being told that it was a work phone number, after receiving a cease and desist letter, and after learning the plaintiff was represented by an attorney.

While not precisely on point, there are two FDCPA cases that represent somewhat similar facts to this case.13In Campbell v. Bradley Fin. Grp., No. CIV.A. 13–604–CG–N, 2014 WL 3350054 (S.D.Ala. July 9, 2014), the defendant repeatedly called the plaintiff, wrongfully alleging that she owed a debt, that she would be sued, and that her wages would be garnished if she did not pay. Campbell, at *4. The plaintiff tried to explain that she had already paid the debt but, because the defendant insisted, she paid the illegitimate debt. Id. Based on the plaintiff’s testimony of her fear of legal action being taken against her, the threatening nature of the phone calls, and the fact that the plaintiff paid the illegitimate debt, the court awarded $15,000 in emotional distress damages. Id.

Similarly, in Gibson v. Rosenthal, Stein, & Associates, LLC, No. 1:12–CV–2990–WSD, 2014 WL 2738611 (N.D.Ga. June 17, 2014), the defendant called the plaintiff and alleged that she owed a debt that she did not owe. Gibson, at *2. The defendant threatened to call the sheriff and have the plaintiff arrested if she did not make a payment. Id. Afraid of going to jail, the plaintiff paid the illegitimate debt using money she needed for living expenses, causing her to go without electricity for two weeks and without water. Id. The court therefore awarded her $15,000. Id.

*13 While these cases are useful as guidance, ultimately, the Court as fact-finder must determine the appropriate amount of damages based on the evidence in this case. Emotional distress damages are particularly difficult to quantify. For example, the Eleventh Circuit pattern jury instructions for emotional distress damages in employment actions contain this language: “You will determine what amount fairly compensates [him/her] for [his/her] claim. There is no exact standard to apply, but the award should be fair in light of the evidence.”Eleventh Circuit Pattern Jury Instructions (Civil) Adverse Employment Action Claims Instructions 4.1, 4.2, 4.3, 4.4, 4.5, 4.9 (2013 Edition).

The Goodins suffered prolonged (over two and a half years) stress, anxiety, and sleeplessness as a result of Bank of America’s misrepresentations regarding the amount of the debt the Goodins owed. This emotional distress reached its peak when the Bank repeatedly threatened the Goodins that, if they did not pay in excess of $15,000, the Goodins’ debt would be accelerated and the Goodins could face foreclosure. The Bank then filed the foreclosure action, and did not dismiss it until six months later (and only after the Goodins were forced to file this lawsuit). While the Goodins did not present evidence from an expert or doctor and in fact did not seek medical attention for their emotional distress, the Court found credible their testimony that they suffered real and severe emotional distress. See supra Part III. Mr. Goodin had worked all his life (Trial Tr. vol. II at 72), but the family was forced into bankruptcy by a poor business investment (Id. at 119). Nevertheless, the Goodins remained ready to continue paying on their mortgage, even while in bankruptcy, but for Bank of America’s gross negligence. While they had other causes of stress as well, their fear of losing their home and feeling of helplessness in the face of Bank of America’s indifference was far and away the primary cause of stress in their lives. Given the facts of this case and the duration of the Goodins’ emotional distress, the Court finds the Goodins are entitled to a larger award than in the mine-run FDCPA case (but nowhere near their request of $500,000 each). Accordingly, the Court, as fact-finder, finds that Mr. and Mrs. Goodin have proven entitlement to $50,000 each for their emotional distress.

- Punitive Damages

In addition to statutory and actual damages, the Goodins request ten million dollars in punitive damages under the FCCPA.14(Doc. 100–1 at 21). The Court may award punitive damages under the FCCPA. Fla. Stat. § 559.77. The Goodins argue that punitive damages are appropriate where the defendant acted with malicious intent, meaning that it did a wrongful act “to inflict injury or without a reasonable cause or excuse.”(Doc. 100–1 at 18) (quoting Story v. J.M. Fields, Inc., 343 So.2d 675, 677 (Fla.Dist.Ct.App.1977). Bank of America likewise cites this standard (Doc. 101 at 16), as have a number of courts that considered punitive damages under the FCCPA, see, e.g., Crespo v. Brachfeld Law Grp., No. 11–60569–CIV, 2011 WL 4527804, at *6 (S.D.Fla. Sept.28, 2011); but see Alecca, 2014 WL 2987702, at *1 (finding unpersuasive the plaintiff’s argument that behavior that had no excuse was equated with malicious intent).

*14 As Bank of America points out, however, Fla. Stat. § 768.72 was amended in 1999, subsequent to the decision in Story, to provide a new standard for punitive damages. Now, “[a] defendant may be held liable for punitive damages only if the trier of fact, based on clear and convincing evidence, finds that the defendant was personally guilty of intentional misconduct or gross negligence.”Fla. Stat. § 768.72(2). Punitive damages may be imposed on a corporation for conduct of an employee only if an employee was personally guilty of intentional misconduct or gross negligence and (1) the corporation actively and knowingly participated in that conduct; (2) the officers, directors, or managers of the corporation knowingly condoned, ratified, or consented to the conduct; or (3) the corporation engaged in conduct that constituted gross negligence and that contributed to the loss suffered by the claimant. § 768.72(3).“ ‘Intentional misconduct’ means that the defendant had actual knowledge of the wrongfulness of the conduct and the high probability that injury or damage to the claimant would result and, despite that knowledge, intentionally pursued that course of conduct, resulting in injury or damage.”§ 768.72(2)(a).“ ‘Gross negligence’ means that the defendant’s conduct was so reckless or wanting in care that it constituted a conscious disregard or indifference to the life, safety, or rights of persons exposed to such conduct.”§ 768.72(2)(b). Barring the application of certain exceptions not present here, any punitive damages award is limited to the greater of: “Three times the amount of compensatory damages awarded to each claimant entitled thereto” or $500,000. § 768.73(1).

Those cases that have applied the Story standard subsequent to the amendment to § 768.72 have not addressed § 768.72. See, e.g., Montgomery, 2008 WL 3540374, at *10. The Goodins contend that the punitive damages provisions of § 768.72 et seq. do not apply to this case because those provisions are in the “Torts” section of the Florida code rather than the “Consumer Collection Practices” section where the FCCPA is. However, the punitive damages section applies to “any action for damages, whether in tort or in contract.”Fla. Stat. § 768.71. Thus, the Eleventh Circuit has assumed that the punitive damages cap in Fla. Stat. § 768.73(1)(a) applies to FCCPA cases. McDaniel v. Fifth Third Bank, 568 F. App’x 729, 732 (11th Cir.2014). A number of other courts have also assumed that the procedural requirements in § 768.72 would apply to FCCPA actions if they did not conflict with the Federal Rules of Civil Procedure. See, e.g., Brook v. Suncoast Sch., FCU, No. 8:12–CV–01428–T–33, 2012 WL 6059199, at *5 (M.D.Fla. Dec.6, 2012).15 As such, the Court will apply the punitive damages standard dictated by the statute. Cf. City of St. Petersburg v. Total Containment, Inc., No. 06–20953–CIV, 2008 WL 5428179, at *25–26 (S.D.Fla. Oct.10, 2008)report and recommendation adopted in part, overruled in part sub nom. City of St. Petersburg v. Dayco Products, Inc., No. 06–20953, 2008 WL 5428172 (S.D.Fla. Dec.30, 2008) (applying § 768.72’s provisions instead of the common law standard laid out in White Const. Co. v. Dupont, 455 So.2d 1026, 1028–29 (Fla.1984)).

*15 As well documented in earlier sections of these findings, the Bank employees were inattentive, unconcerned, and haphazard in their repeated and prolonged mishandling of the Goodins’ loan. Then, the auditor whose very job it is to correct errors, was himself negligent in his review of the Goodins’ file. If that was the sum of Bank of America’s actions, it would be guilty of negligence many times over, but perhaps not gross negligence.

It is the Bank’s employees’ failure to respond to the Goodins’ many efforts to correct the Bank’s errors that sets this case apart. Bank of America received numerous communications from the Goodins and their attorney explaining the problems with the Bank’s servicing. (Joint Ex. 5 at 2; Joint Ex. 6 at 37, 39, 40; Pl.’s Ex. 23). Yet, beyond noting that the communications were received, the Bank employees did nothing to correct the servicing errors. With their home at stake, the Goodins might as well have been talking to a brick wall.

In taking no action to prevent the errors from continuing, even after being repeatedly notified of them, the Bank employees’ conduct was so wanting in care that it constituted a conscious disregard and indifference to the Goodins’ rights. It was as if the Goodins did not exist. Because the Bank’s employees disregarded the Goodins’ complaints, the servicing errors continued unabated, the Bank continued to send the Goodins false information about the amount of their debt, and then the Bank filed a misbegotten foreclosure action. The Bank employees’ continued gross negligence was only stopped by the filing of this federal lawsuit.

Moreover, in creating a system where one Bank department did not communicate with another, where there were inadequate internal controls to ensure statements provided correct information, and where there was no way for Bank customers to get the attention of the Bank to correct the Bank’s errors, the Bank engaged in grossly negligent conduct. As such, it should be held liable for punitive damages for its employees’ gross negligence.

In justifying their request for $10 million in punitive damages, the Goodins cite to only one case they believe to be similar, Toddie v. GMAC Mortgage LLC, No. 4:08–cv–00002, 2009 WL 3842352 (M.D.Ga. March 26, 2009), where the Court awarded $2,000,0001 in punitive damages and $570,000 in compensatory damages. (Doc. 100–1 at 19–20).Toddie, however, was a wrongful foreclosure and breach of contract case, not an FCCPA case, and involved much more egregious facts, as the defendant actually foreclosed on the plaintiff’s home.

Where courts have awarded punitive damages in FCCPA cases, the amounts have typically been small. See Rodriguez, 2009 WL 535980, at *6 (awarding $2,500 in punitive damages); Montgomery, 2008 WL 3540374, at *11 (awarding $1,000 in punitive damages); Barker, 2006 WL 1679645, at *3 (awarding $10,000 in punitive damages).16 However, this case presents a different situation, one of a very large corporation’s institutional gross negligence.

*16 The goal of punitive damages is to punish gross negligence and to deter such future misconduct. Thus, the award must be large enough to get Bank of America’s attention, otherwise these cases become an acceptable “cost of doing business.” Bank of America is a huge company with tremendous resources, a factor that the Court may and has considered in determining an appropriate award. See Myers v. Cent. Florida Investments, Inc., 592 F.3d 1201, 1216 (11th Cir.2010).17 Also, this is a serious FCCPA case, in which there were a large number of violations that occurred over a long period of time, and in which the Bank ignored the Goodins’ repeated attempts to fix its many errors. The Court, as fact-finder, finds that the Goodins have proven by clear and convincing evidence that a punitive damages award of $100,000 is appropriate.18

Goodin v. Bank of Am., N.A., No. 3:13-C

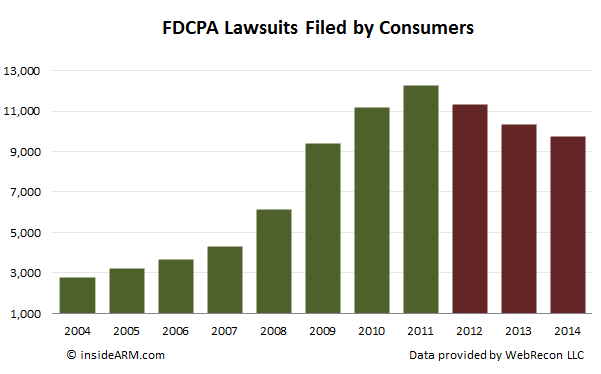

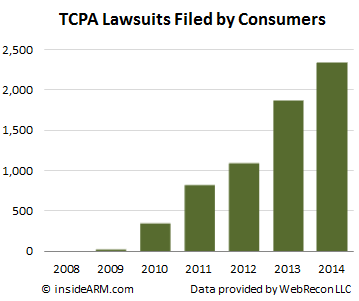

While still far below the total volume of FDCPA suits – there were 2,336 TCPA suits filed in 2014 – the increased focus on the telephone communications statute has left many ARM companies scrambling to bring their operations into sharper compliance.

While still far below the total volume of FDCPA suits – there were 2,336 TCPA suits filed in 2014 – the increased focus on the telephone communications statute has left many ARM companies scrambling to bring their operations into sharper compliance.

![ba080410-lawsuit-vs-lenders-class-action-lawsuit43[1]](https://timothymccandless.files.wordpress.com/2012/04/ba080410-lawsuit-vs-lenders-class-action-lawsuit431.jpg)

Debtors and obligors might remind the court that any awards are taxable and non-deductible to them. Conversely, awards against creditors are expenses that offset taxes paid by creditors.